Editor’s note: Dr. Gerald Cohen is Chief Economist, Kenan Institute of Private Enterprise.

+++

CHAPEL HILL – Debt ceiling crises have become increasingly commonplace in the last decade and a half. Even as the June deadline grows closer, there is a sense of déjà vu around the type of policy discussion such crises engender. Just as in 2011, 2013 and 2021, policymakers and pundits tend to focus on the risk of catastrophic default. And, just as in previous crises, I anticipate an agreement to raise the ceiling will eventually be struck, averting a total collapse in U.S. credit. This debate, however, often fails to acknowledge an essential point: The debt ceiling drama itself is bad for the economy. What is more, as I describe below, the effects this time around may be particularly detrimental to U.S. economic performance in the months and years to come.

Dr. Gerald Cohen (UNC-CH photo)

Even if the debt limit were increased today, the uncertainty created by the impending debt ceiling deadline has already raised the cost of borrowing and is impeding some hiring and investment. Moreover, an agreement will probably entail some decline in government spending, which will worsen an economic slowdown (which we predict to be on its way). And, while this belt-tightening will stave off total default, it fails to solve the real problems driving our debt dynamics – making us more likely to encounter this situation again in the future.

By itself, the risk of potential default raises interest costs for the entire economy. Historically, the U.S. is seen to have the least risky credit in the world. Subsequently, the rate of return on U.S. Treasurys is generally known as the “risk-free rate” and serves as the benchmark for other interest rates. Thus, business loans and mortgages are priced based on a spread to Treasurys, with riskier loans paying a higher interest rate versus the underlying Treasury rate. So, if Treasury interest rates go up, even if risks of business or household defaults don’t change, business loan and mortgage interest rates will rise. As a result, housing and business activity will slow.

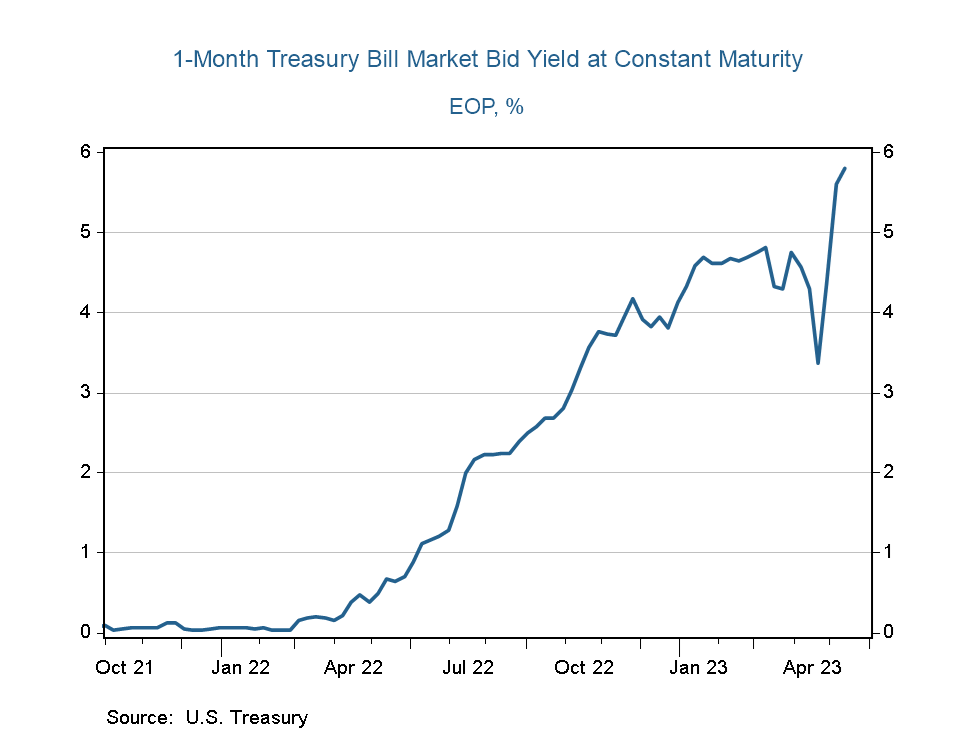

This increase in the risk-free rate can be seen in the chart below. The general rise in 1-month Treasury interest rates over the last year is the result of the Fed increasing interest rates, but the recent spike in 1-month rates is the result of debt ceiling concerns. That’s because market participants have priced in some probability that the debt won’t be repaid (or, in the case of the invocation of the 14th Amendment, that new debt might not be honored).

This risk premium is not new. The Government Accountability Office estimated that the 2011 debt ceiling standoff – which ultimately led to Standard & Poor’s downgrading U.S. debt – cost the Treasury $1.3 billion in 2011 alone. Since the Treasury had to issue longer-dated debt at elevated interest rates, the total costs were meaningfully higher. The 2013 debt ceiling kerfuffle was a bit less dramatic, although some large investors, such as Fidelity, reported that their money market mutual funds refused to hold Treasurys maturing immediately after the potential default date. As a result, the GAO estimated that the debt limit standoff in 2013 cost the federal government between $38 million and $70 million in higher borrowing costs.

Uncertainty around the willingness of the U.S. government to pay its bills also impedes business decisions. Research has shown that policy and regulatory uncertainty hampers investment, especially in projects that are dependent on government spending. These projects with some dependence on the U.S. government constitute a much larger slice of the economy than you might imagine. Direct federal spending is roughly 7% of GDP, while total federal spending, including social insurance and grants to states, was 25% of GDP in 2022. The policy uncertainty also has a meaningful deleterious impact on decisions to invest in projects that are hard to reverse – such as the decision to spend $100 billion over 20 years to build a new semiconductor manufacturing center – and these projects are often the ones that have the longest economic tails.

Many market participants now believe that even if Congress strikes an agreement in the eleventh hour, the current impasse is likely to lead to other credit agencies aside from S&P downgrading United States debt. This would likely mean a long-term increase in the risk premium on Treasury securities. Thus, in contrast to previous events, the higher borrowing costs will not be a temporary blip, but a more permanent rise in the interest rates the U.S. government would pay – which would likely bleed into higher interest costs for the U.S. economy as described above. Moreover, since a large component of the U.S. economy depends on federal spending, U.S. businesses are likely to be perceived as riskier, which will raise their borrowing costs even further. A potentially even more damaging consequence would be that international investors shift away from the dollar as the world’s “reserve currency,” lessening demand for U.S. assets and having further negative consequences for U.S. interest rates, the dollar and our ability to finance large trade deficits.

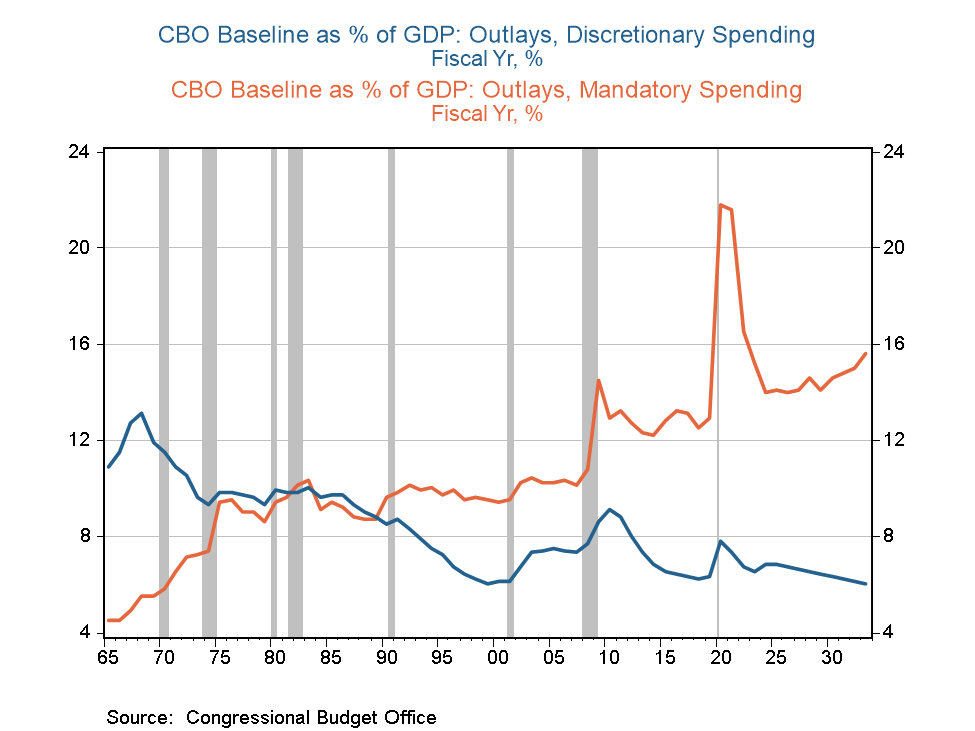

Current negotiations revolve around spending cuts as a means to lower the long-term deficit. There are two errors in this thinking. First, if the U.S. economy is slowing, as most forecasters believe – or headed toward a recession, as I believe – cuts in federal spending now would exacerbate the slowdown. This is one of the lessons learned from 2011, when debt-ceiling-negotiated fiscal restraint slowed the already tepid recovery from the 2008-09 Great Recession. Second, the discussions center around discretionary spending – i.e., spending on defense, education and scientific research grants. As the chart below illustrates, this is not the source of our increased deficits. In fact, even without the proposed cuts, this category is expected to contract to its lowest level (relative to the size of the economy) on record (excluding defense, the story is the same). Serious negotiations should tackle the real culprits – increased mandatory spending on Social Security and in particular healthcare, as well as flat revenue, expected to remain unchanged at roughly 18% of GDP over the period.

Most countries believe that when a government makes decisions about the path of expenditures and revenue, there is no need to revisit the resultant impact on the debt, because that is a consequence of budget decisions that were made long ago (as well as unforeseen economic events). Unfortunately, the U.S. is one a very few countries that has a debt ceiling, and it seems to have become the focal point of long-term debt sustainability discussions. While I welcome these discussions, we should not be having them as part of the annual budget negotiations – and certainly not as the U.S. government faces default. Holding hostage the full faith and credit of the U.S. has serious consequences for the economy, and this latest installment of the debt ceiling drama may demonstrate just how serious those consequences can be.

(C) Kenan Institute of Private Enterprise

This post was originally published at https://kenaninstitute.unc.edu/commentary/debt-ceiling-drama-another-brick-in-the-recession-wall/