Since my first article for ExitEvent in May 2014 analyzed North Carolina’s entrepreneurial community through a data lens, it felt fitting that my last piece would do the same. And yet, I struggled with writing this piece. Not because it was bittersweet (which in fact it is), but because in looking through several sets of data, I was disappointed and didn’t want to be the bearer of bad news.

But it’s not all bad news, and benchmarking the region against itself and other regions is important if the Triangle is going to grow as an entrepreneurial ecosystem. Regardless, a lot has changed since 2014 that’s worth investigating.

For starters, the data available to measure the strength of the state’s startup ecosystem has changed drastically. The number of reports, data collections, and sheer number of groups measuring stats like new company formation, fundraising, job creation and IP has multiplied tenfold. For example, The Kauffman Index—a long standing source of measuring entrepreneurial ecosystems—tripled in size and scope. It went from one index to three, and the foundation began publishing data at the state, region and MSA levels. It’s good news for the state and Triangle region—more data is always better.

Here locally, the Council for Entrepreneurial Development (CED) began collecting its own data on funding events around the state and reporting the results in aggregate quarterly. Lewis Sheats, professor and executive director of the North Carolina State University E-Clinic now conducts a quarterly survey to gauge entrepreneur optimism. And both of the region’s largest home-grown tech hubs, American Underground and HQ Community, began collecting and publishing data from their members’ to track progress.

The Triangle’s universities have ramped up entrepreneur-focused initiatives over the past few years too, and all have doubled down on reporting.

First, the good news

By all measures that I checked out over the last week, North Carolina is doing better today in attracting venture capital and launching new startups than in 2014.

Total North Carolina Venture Capital Raised by sector, 2013-2017; Data Source: CED

Venture capital investments rose significantly over the four-year period. According to CED’s Innovator’s Report, tech and life science investments—which historically make up the lion’s share of investment in the state—rose dramatically since 2013. Cleantech and advanced manufacturing investments have stayed roughly the same.

According to the same data, 2015 was the biggest year for the state with $1.18 billion raised across all sectors. With $768 million raised in the first three quarters of 2017, funding is on track to match or beat 2016, but it’s unlikely to reach the heights of 2015.

In Kauffman’s indices, North Carolina shows growth in most measures. More entrepreneurs start businesses today than in 2013, though fewer of those new entrepreneurs start up because they are unemployed. Most entrepreneurs are opportunistic. Startups are also staying alive longer. And they make up a larger share of all businesses in North Carolina.

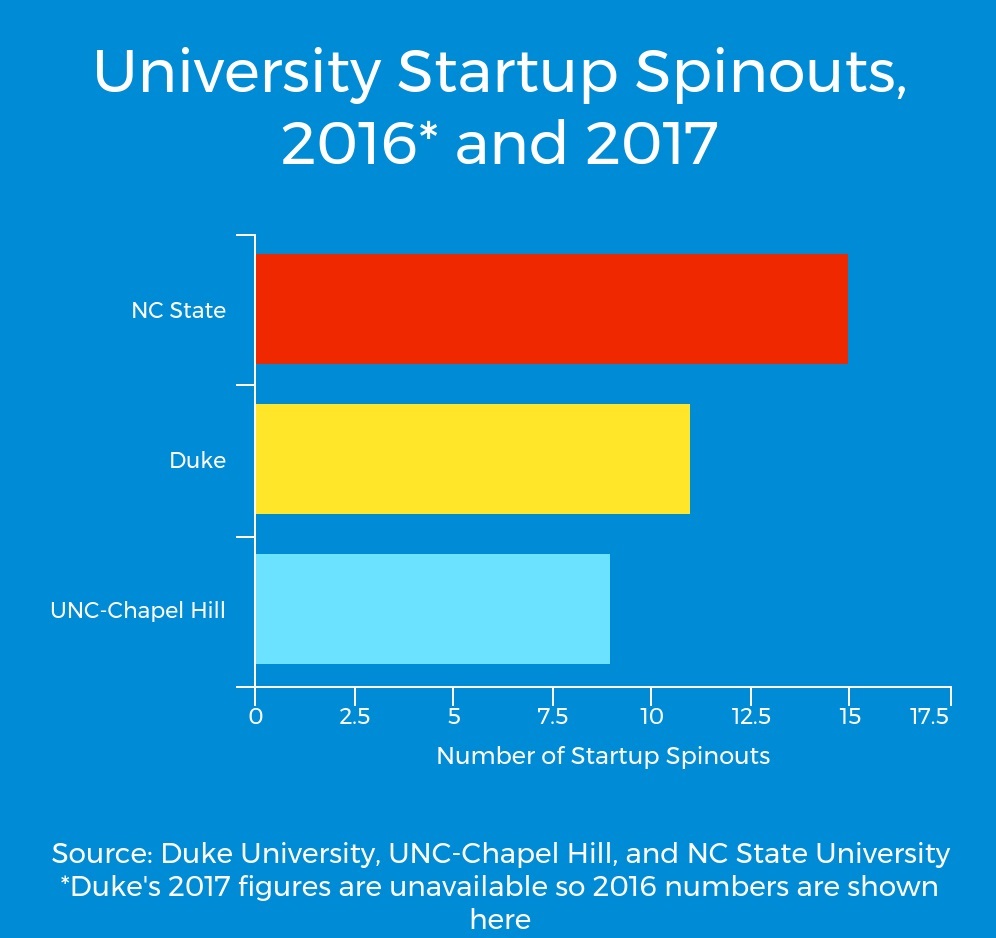

The region’s universities are churning out more startups today than in 2013 too. Duke alone spun out 11 new startups in 2016. Meanwhile, NC State spawned 15 new startups in FY 2017 (up from 8 in 2013), and UNC-Chapel Hill spun out nine.

University Startup Spinouts 2016 & 2017

Some Tough Love

Now time for the not-so-good news. While there are more North Carolina startups, more of which have raised money and at larger check sizes, the same is true of the rest of the country and many peer states and regions. And compared to those, the state treads water—sometimes bobbing up and other times sinking down.

For example, in the Kauffman Startup Activity index, which measures new business creation and activity, North Carolina shifted down to 9th place from 8th among large states in 2016. And in its Growth Entrepreneurship index, the state dropped from 8th to 18th place, meaning startups in our state are not growing as quickly as those in others. There’s also less density and fewer ‘scale-ups’ as in other states during the measured time. Granted, the last time data was collected for the growth index is 2014—it does not capture the recent growth of companies like Pendo, Mati Energy or TransLoc. But even so, the large drop is troubling.

When looking at venture capital, it’s even more apparent that North Carolina’s increases in funds raised aren’t big enough to place it in the top 10. For example, for Q3 2017, with $188.94 million raised, NC ranks 15th out of the 47 reporting states. And yet, $188 million isn’t a poor quarter for North Carolina—it’s a decent showing. For context, it’s not much less than the state’s average quarterly raise—$206.28 million.

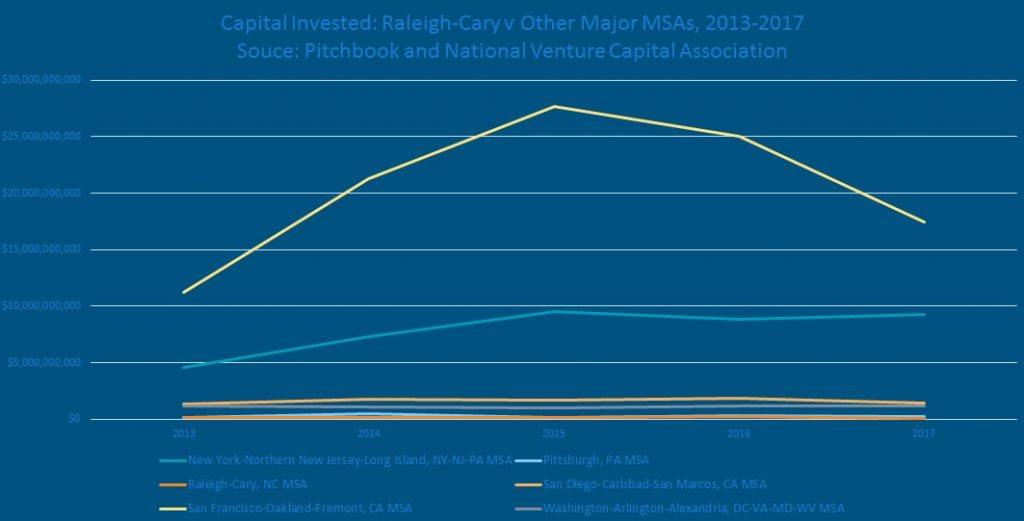

And when we drill down into Raleigh-Cary, the only NC Metropolitan Statistical Area (MSA) included in the National Venture Capital Association (NVCA) quarterly reports, dollars raised look even more paltry compared to the other top 25 MSAs.

Raleigh-Cary vs. other MSAs in Capital Investment, 2013-2017; Data Source: Pitchbook and NVCA

Any way you slice and dice the data, Raleigh-Cary’s raises barely register on the map. In comparison to the largest tech hubs—New York, the Valley and Washington DC—Raleigh-Cary looks like a blip on the screen.

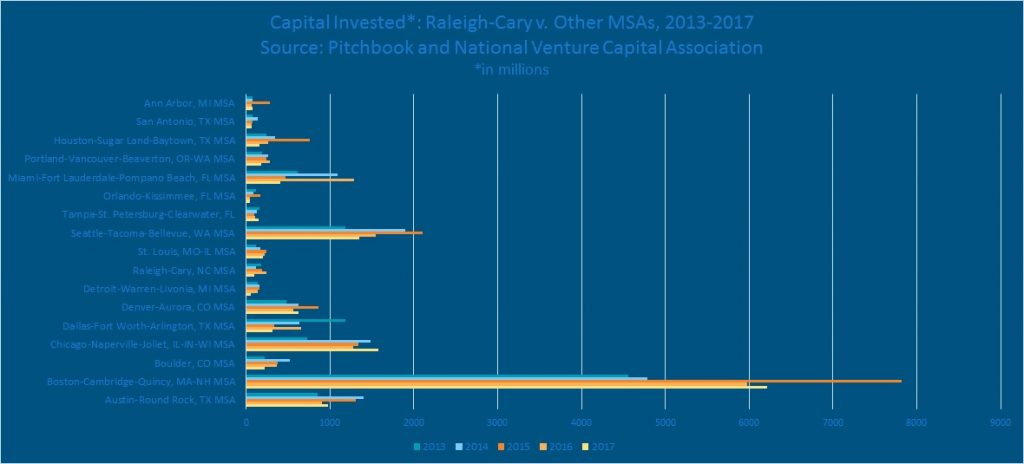

Compared to smaller MSAs, Raleigh-Cary begins to show some life, but funding totals align with regions like St. Louis, Detroit, Portland, Ore. and San Antonio rather than cities we like to be compared to, like Boston or Austin.

Raleigh-Cary v smaller MSAs, 2013-2017; Data Source: Pitchbook and NVCA

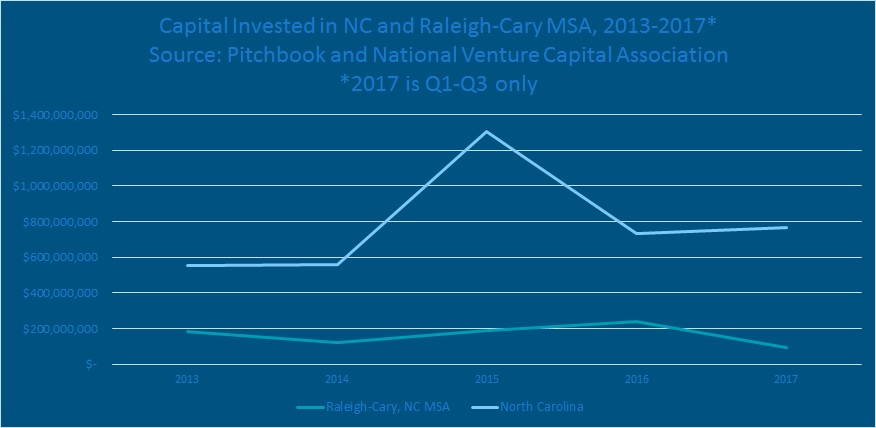

When the data are side-by-side, it’s clear Raleigh-Cary’s capital raised contributes a large share to North Carolina’s overall capital raised. But the gap between the two is evident, meaning other regions and cities—like Durham and Charlotte—contributed to North Carolina’s overall figures, but aren’t reported by the NVCA. Perhaps, if MSAs were defined differently and Raleigh-Cary was actually Raleigh-Cary-Durham-Chapel Hill, it would stack up against the larger MSAs. But as it stands, the lone North Carolina representative on the NVCA’s fundraising break-down by MSA is pretty average compared to the country’s largest regions.

Raleigh-Cary and NC, 2013-2017; Data Source: Pitchbook and NVCA

What’s Next?

The state’s entrepreneurial activity over the past few years is certainly worth celebrating. It’s an accomplishment to have so many new companies forming, creating jobs, rewarding investors and supporting the state’s economy. But it’s also important to note that other states are growing strong ecosystems too. And when compared to them, North Carolina hovers between an 8th and 20th ranking depending on the metric.

Taking a hard look at each of these metrics moving forward would help the state and regions better allocate resources and prioritize programs.

The final quarter of 2017 would also be a good time for state and regional leaders to determine what areas of growth are most important for North Carolina’s economic future. Does the state want to lead the nation in venture capital investments? Or is maintaining a steady but mid-level rank satisfactory? Is it important for the state to increase the number of new startups birthed each year instead? Or should focus be on the sustainability and scale-up of existing startups?

Finally, what measures are missing? The Triangle region has loudly and intently focused on increasing diversity throughout the entire entrepreneurial ecosystem. And yet, who is tracking that progress at a regional level?

Should there be tracking for quality of life—an increasingly important factor in attracting quality talent to the state? Or job creation—NC IDEA, HQ Community and the American Underground all track the jobs their members or graduates create, but who will aggregate these and add new data to capture all the job creation occurring outside the hubs?

And who should and will be willing to track, compile and publish these data? It’s a large, difficult, but increasingly more important job if the different tech regions and the state want to increase its standings among peers.